In this question, the Bright Company has experienced a favorable labor rate variance of $45 because it has paid a lower hourly rate ($5.40) than the standard hourly rate ($5.50). The combination of the two variances can produce one overall total direct labor cost variance. Predictive analytics is another powerful tool for managing labor variance. By leveraging machine learning algorithms, companies can predict future labor costs and variances based on historical data and external factors like market conditions. This proactive approach enables companies to make informed decisions about staffing, training, and resource allocation before variances occur.

- Standard costs are used to establish theflexible budget for direct labor.

- Minimizing labor variance requires a multifaceted approach that integrates both proactive and reactive strategies.

- Labor variances also have implications for budgeting and forecasting.

- Labor rate variance is the difference between actual cost of direct labor and its standard cost.

- The standard rate per hour is the expected hourly rate paid to workers.

How can companies reduce Direct Labor Mix Variance?

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. 11 Financial is a registered investment adviser located in Lufkin, Texas. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. 11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links.

How Do Companies Decrease Direct Labor Mix Variance?

This information gives the management a way tomonitor and control production costs. Next, we calculate andanalyze variable manufacturing overhead cost variances. In this example, the Hitech company has an unfavorable labor rate variance of $90 because it has paid a higher hourly rate ($7.95) than the standard hourly rate ($7.80). If we compute for the actual rate per hour used (which will be useful for further analysis later), we would get $8.25; i.e. $325,875 divided by 39,500 hours. We have demonstrated how important it is for managers to beaware not only of the cost of labor, but also of the differencesbetween budgeted labor costs and actual labor costs.

Rate Variance and Efficiency Variance

Conversely, favorable variances might indicate underutilization of labor resources, which could be a red flag for potential operational inefficiencies or overstaffing. The labor variance is particularly suspect when the budget or standard upon which it is based has no resemblance to actual costs being incurred. The use of the labor variance is questionable in a production environment, for two reasons. First, other costs usually comprise by far the largest part of manufacturing expenses, rendering labor immaterial.

Advantages and Disadvantages of Direct Labor Mix Variance

In this case, the actual rate per hour is $9.50, the standard rate per hour is $8.00, and the actual hours worked per box are 0.10 hours. This is an unfavorable outcome because the actual rate per hour was more than the what are temporary accounts fanda glossary standard rate per hour. As a result of this unfavorable outcome information, the company may consider using cheaper labor, changing the production process to be more efficient, or increasing prices to cover labor costs.

The total direct labor variance is also found by combining the direct labor rate variance and the direct labor time variance. By showing the total direct labor variance as the sum of the two components, management can better analyze the two variances and enhance decision-making. With either of these formulas, the actual hours worked refers to the actual number of hours used at the actual production output.

Labor hours used directly upon raw materials to transform them into finished products is known as direct labor. This includes work performed by factory workers and machine operators that are directly related to the conversion of raw materials into finished products. DLYV can be affected by several factors, such as labor rate or wage changes, variations in employee skill levels, differences in the number of hours worked, and changes in working conditions. Additionally, labor mix variance plays a role, particularly in environments where multiple types of labor are employed. This variance occurs when the proportion of different labor categories used deviates from the standard mix. For example, if a project requires a higher proportion of skilled labor than initially planned, the labor mix variance will reflect this shift, potentially leading to higher costs.

Each bottle has a standard labor cost of \(1.5\) hours at \(\$35.00\) per hour. Calculate the labor rate variance, labor time variance, and total labor variance. Each bottle has a standard labor cost of 1.5 hours at $35.00 per hour.

The most common causes of labor variances are changes in employee skills, supervision, production methods capabilities and tools. An example is when a highly paid worker performs a low-level task, which influences labor efficiency variance. It is always important, as you are starting to see, to look at all options as we work through management decisions. Companies can reduce Direct Labor Mix Variance by more accurately predicting labor needs, using flexible staffing solutions, and making use of labor-saving technology. Additionally, it is important to ensure that labor costs are monitored and managed effectively. Direct Labor Mix Variance typically occurs when the actual labor mix used in production is different from what was budgeted or anticipated.

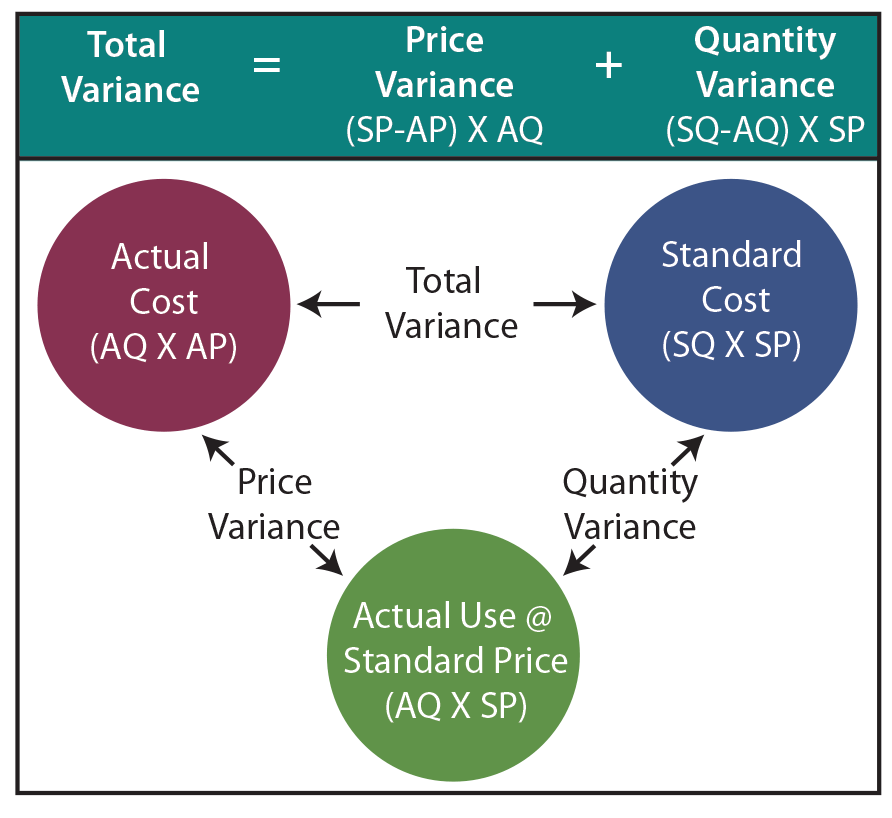

There are two components to a labor variance, the direct labor rate variance and the direct labor time variance. Figure 10.43 shows the connection between the direct labor rate variance and direct labor time variance to total direct labor variance. In this case, the actual hours worked are 0.05 per box, the standard hours are 0.10 per box, and the standard rate per hour is $8.00. This is a favorable outcome because the actual hours worked were less than the standard hours expected. Labor variance is a multifaceted concept that encompasses several key components, each contributing to the overall difference between expected and actual labor costs. One primary element is the labor rate variance, which arises when there is a discrepancy between the standard wage rate and the actual wage rate paid to employees.